International Bank Transfer: Impact on Expats’ Money

Sending money home from the United States to the Philippines often feels more complicated than it should be, especially when you want every dollar to count for your family. Many Filipino expatriates rely on international bank transfers, yet myths about speed, fees, and safety create real confusion. By breaking down the complex systems and common misconceptions behind global money movement, you can confidently choose secure, cost-effective ways to support loved ones without losing out to hidden charges.

Table of Contents

- International Bank Transfer Basics And Misconceptions

- Types Of International Transfers And Key Distinctions

- How International Bank Transfers Work Securely

- Legal Compliance, Regulations, And KYC Requirements

- Fees, Risks, And Fintech Alternatives Compared

Key Takeaways

| Point | Details |

| Understand Fee Structures | Different fee models can significantly impact how much your recipient actually receives; always clarify fee responsibility before initiating a transfer. |

| Utilize Transparent Platforms | Consider fintech options that provide lower fees and real-time exchange rates; this can result in significant savings. |

| Verify Sender Details | Always double-check recipient information with your family before sending money to avoid costly mistakes. |

| Be Aware of Security Risks | Protect your information from phishing and scams; use official channels to send money and verify details directly for safety. |

International bank transfer basics and misconceptions

When you send money back to your family in the Philippines, you’re participating in one of the world’s oldest financial systems. International bank transfers aren’t random magic—they follow established pathways and rules. Yet most people operate with incomplete or flat-out wrong information about how their money actually moves.

Let’s start with what’s actually happening when you hit “send.”

What happens behind the scenes

Your transfer isn’t a direct flight from your American bank account to your relative’s account in Manila. Instead, your money travels through multiple intermediary banks that act as checkpoints and validators. Think of it like a package moving through different delivery hubs before reaching the final address.

The process relies on established systems that govern complex methodologies and regulations in global finance. Your bank uses codes and identifiers to ensure funds reach the correct destination without getting lost in translation.

Two key systems power international transfers:

- SWIFT: A messaging network that banks use to communicate transfer instructions securely to each other across borders

- IBAN: An International Bank Account Number that identifies specific accounts in participating countries

Your Filipino bank account may not have an IBAN (the Philippines uses a different system), which is why transfers there often require additional routing information or intermediary banks.

Common misconceptions that cost you money

Here’s where reality diverges from what you probably think:

- “My bank quoted me the official exchange rate”: Banks apply hidden markups to exchange rates. What they advertise and what you actually get are different numbers.

- “Faster transfers cost more”: Speed depends on the pathway, not a premium fee. Some routes are slow by design, not pricing.

- “My recipient pays the fee, not me”: Both sender and receiver fees exist. Your bank charges you; their bank charges them. You’re often covering both costs unknowingly.

- “All transfers take the same time”: Routing varies dramatically. A transfer to Metro Manila takes different paths than one to a provincial bank.

Most Filipino expatriates overpay by 3-8% annually when using traditional banks for remittances, even without realizing they’re paying multiple hidden fees.

Why this matters for your remittances

You’re sending real money to real people. A $500 transfer might become $480 in your mother’s account after fees and markups pile up. Over a year, that’s thousands of dollars lost.

Understanding how transfers work helps you spot better options and avoid unnecessary costs. You deserve to know where your money goes and what it costs.

Pro tip Ask your bank for their SWIFT code and the exact exchange rate they’re applying to your next transfer—compare it to real-time rates on Google or XE.com to see what markup you’re actually paying.

Types of international transfers and key distinctions

Not all international transfers work the same way. The path your money takes depends on where it’s going, how fast you need it, and who pays the fees. Understanding these distinctions can save you hundreds of dollars annually on remittances to the Philippines.

Transfers fall into distinct categories based on geography, speed, and cost responsibility.

Geographic boundaries matter

Domestic transfers stay within the United States. International transfers cross borders. But within international transfers, geography creates different rules.

European transfers use SEPA, a streamlined system for countries in the Eurozone. SEPA transfers are faster and cheaper because the infrastructure is unified. However, if you’re sending to the Philippines, SEPA doesn’t apply—you need a global system.

Most transfers outside Europe use SWIFT, the worldwide standard. SWIFT transfers work globally but move slower because they pass through multiple intermediary banks.

Here’s a comparison of international transfer systems and their impact on remittances to the Philippines:

| System Used | Applicability | Typical Speed | Cost Impact |

| SWIFT | Global (inc. Philippines) | 2-5 business days | Multiple fees, higher cost |

| SEPA | Eurozone/Europe only | Same/next day | Low fees, not available for Philippines transfers |

| Fintech Platforms | Global (varies) | Same/next day | Lower fees, better rates |

Fee structures determine your actual cost

Here’s what most people miss: different fee structures exist based on who bears the expense. This changes what you actually send and what arrives.

Three fee models apply:

- OUR: You (the sender) pay all fees. Your recipient gets the full amount minus what your bank charged. Most expensive for you.

- BEN: Your recipient pays all fees. You send the amount you intend, but their bank deducts charges. Cheaper for you, but your family receives less.

- SHA: Both parties split the fees. Middle ground, though transparent communication matters here.

When you send $500 OUR to the Philippines, after your bank’s fee ($15) and intermediary charges ($10), you’re sending $475. Your recipient gets whatever arrives after their bank takes a cut.

Speed versus cost tradeoffs

Fast transfers usually cost more because they skip certain intermediary banks. Standard transfers are slower but cheaper. Express options exist but aren’t always worth the premium for family remittances.

Most Filipino expatriates default to OUR transfers through traditional banks, paying 5-7% in total fees without realizing faster, cheaper alternatives exist.

One-time versus recurring transfers

If you send money monthly, some platforms offer better rates for recurring transfers. One-time transfers typically have higher per-transaction costs.

Pro tip Always request SHA or negotiate OUR with transparent fee disclosure before sending—ask your bank for the complete fee breakdown, including intermediary charges, so you know exactly what your family receives.

How international bank transfers work securely

Your money crossing borders might sound risky, but international bank transfers are actually among the safest financial transactions you can make. Banks have spent decades building systems specifically designed to protect your money and ensure it arrives exactly where it should go.

Here’s how security actually works behind the scenes.

The verification process starts before anything moves

When you initiate a transfer, your bank doesn’t just accept your request. They verify your identity, confirm the recipient details, and check that everything matches their records. This initial screening catches most fraud before it starts.

You’ll provide your recipient’s name, bank name, account number, and routing information. Your bank cross-references this data to ensure accuracy. A single mistake in these details can send money to the wrong account, so banks triple-check.

Encryption protects your information in transit

Once verification passes, your transfer request enters encrypted messaging networks like SWIFT. Think of encryption as a secure envelope that scrambles your financial information into unreadable code during transmission.

Only the intended recipient bank can decrypt this message. Even if someone intercepts it, they see gibberish. Without the encryption key, your bank account numbers and transfer amounts remain invisible to unauthorized parties.

Regulatory oversight creates accountability

Banks aren’t free to do whatever they want. Government agencies monitor international transfers for compliance with anti-money laundering regulations. If a transfer looks suspicious—like unusually large amounts or patterns suggesting fraud—it triggers an automatic review.

This monitoring protects you. It means your bank is held legally accountable if they fail to prevent fraud or allow unauthorized transfers.

Multiple checkpoints along the route

Intermediaries banks that handle your transfer apply their own security checks:

- Verify sender and receiver information matches

- Flag transfers that deviate from normal patterns

- Monitor for sanctions violations and terrorist financing risks

- Apply their own encryption standards

Each checkpoint reduces the chance something goes wrong.

Why this matters for Philippine remittances

When you send money to your family, robust regulatory oversight and encryption mean your family’s account is protected. Your recipient won’t receive money belonging to someone else, and no one can intercept your transfer mid-journey.

Bank wire transfers have fraud rates below 0.1% globally because of these layered security systems—far safer than sending cash or using unregulated money services.

What you should actually worry about

The real risk isn’t the bank system—it’s you. Phishing emails, fake bank websites, and social engineering cause most transfer fraud. Someone tricks you into revealing your login credentials or authorization codes.

Only use official bank websites and apps. Never click links in emails claiming to verify your account. Call your bank directly if you’re unsure.

Pro tip Verify recipient details with your family directly before submitting any transfer—call them or use WhatsApp to confirm their account number, bank name, and spelling of their name matches exactly what you’re sending to.

Legal compliance, regulations, and KYC requirements

When you send money internationally, you’re not just moving your own funds—you’re participating in a regulated financial system. Governments worldwide have strict rules about money transfers to prevent illegal activities. Understanding these requirements protects you and ensures your transfers proceed smoothly.

Compliance isn’t bureaucratic red tape. It’s the system that keeps criminals and terrorists from hiding money through international transfers.

What KYC actually means

Know Your Customer, or KYC, requires financial institutions to verify who you are before processing transfers. Banks collect your name, address, identification documents, and sometimes your occupation or source of funds. This seems invasive, but it’s the legal requirement everywhere.

The purpose is straightforward: prevent money laundering and terrorist financing. If banks don’t know who you are, they can’t detect suspicious patterns.

The verification steps you’ll encounter

When you open an account or initiate large transfers, banks follow a standardized process:

- Collect your personal identification (passport, driver’s license, national ID)

- Verify your address using utility bills or official documents

- Confirm your source of funds (employment, business, investments)

- Document the purpose of your transfer

- Cross-reference your information against government watchlists

This process takes time. Don’t rush it or provide false information—that’s illegal and triggers investigation.

Anti-Money Laundering monitoring never stops

After your transfer is processed, compliance systems continue monitoring transactions for unusual patterns. If you suddenly transfer $50,000 monthly when your typical transfer is $500, that triggers a review. Banks must report suspicious activities to government agencies.

This ongoing monitoring protects you. It means your family’s account can’t be used for illegal purposes without detection.

Regulations vary by country but follow core principles

Global KYC regulations require customer identification, due diligence, and transaction monitoring. However, specific rules differ between the United States, Philippines, United Kingdom, and Europe.

The United States has stricter rules than many countries. Transfers above $10,000 require additional reporting. International transfers trigger automatic monitoring regardless of amount.

The Philippines requires identification and verification for all transfers above approximately 500,000 Philippine Pesos.

Why non-compliance destroys your access

Banks that fail compliance checks face massive fines and license revocation. Some banks have paid over $1 billion in penalties for inadequate KYC procedures. This means banks err on the side of caution—they’d rather deny your transfer than face legal consequences.

Banks must maintain transparent records and keep up with evolving regulations—failure to comply results in fines, suspended licenses, and criminal charges.

What this means for your remittances

Your bank might request additional documentation for your regular transfers. They might ask why you’re sending money to the Philippines or request recent pay stubs. This is normal and required by law, not discrimination.

Provide the information. It speeds up your transfers and keeps your account active. Refusing or providing false information creates problems.

Pro tip Gather documentation before initiating transfers: valid ID, recent utility bill showing your address, and a simple explanation of why you’re sending money (family support, loan repayment, etc.)—having this ready eliminates delays and repeated requests.

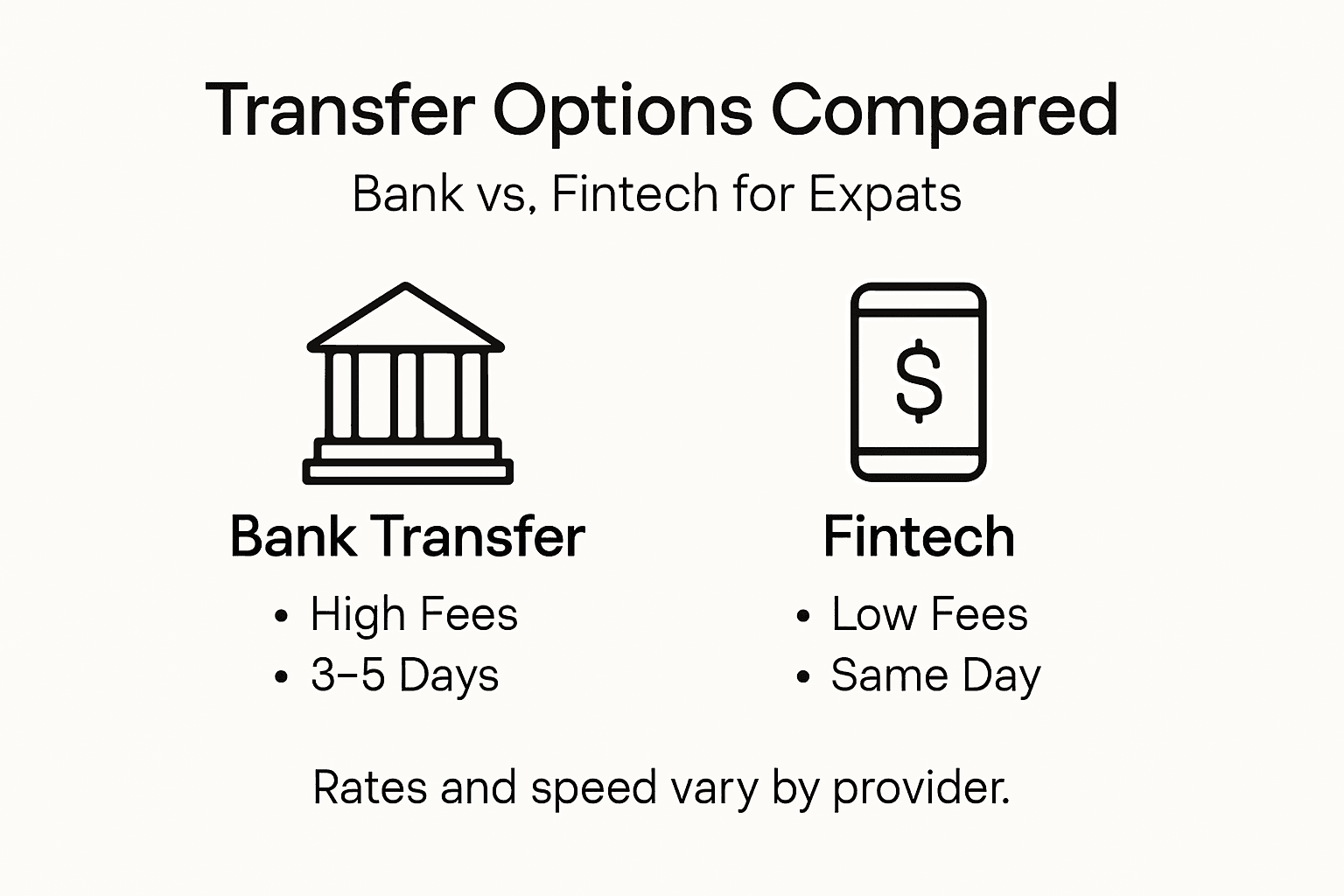

Fees, risks, and fintech alternatives compared

Traditional banks dominate international transfers, but they’re not your only option. Newer fintech platforms challenge the status quo with lower fees and faster processing. Understanding the tradeoffs between banks and alternatives helps you choose wisely for your family remittances.

The choice matters because fees compound. Overpaying by just 3% annually adds up to hundreds of dollars sent to the Philippines.

What traditional banks actually cost

Banks rarely advertise their true fees upfront. You’ll encounter multiple charges stacked together:

- Originating bank fee: $15-50

- Intermediary bank charges: $10-30

- Receiving bank fee: $5-15

- Exchange rate markup: 2-5% (hidden)

- Correspondent bank fees: $10-20

A $500 transfer might cost $80-100 total. That’s 16-20% of your money lost before it reaches your family. Banks profit handsomely from remittances.

The following table summarizes key differences between traditional banks and fintech platforms for international transfers:

| Transfer Method | Fee Range | Speed | Security Level |

| Traditional Bank | $80-100 per $500 | 3-5 business days | FDIC-insured, highly regulated |

| Modern Fintech | $10-15 per $500 | Same/next day | Varies, check licensing |

| Cash-Based Services | $20-30 per $500 | Hours to next day | Lower oversight, higher risk |

Fintech platforms offer different economics

Companies like Wise, Remitly, and Unplex use blockchain-based innovations to reduce costs by eliminating intermediary banks. Instead of routing through multiple institutions, they move money directly using digital networks.

The result: fees drop to 1-3%, and exchange rates stay closer to real-time rates. A $500 transfer costs $10-15 instead of $80.

But fintech carries different risks

Newer platforms mean less regulatory history. Some operate in gray areas legally. If a fintech company fails, your money might be trapped in accounts you can’t access.

Bank transfers, despite high fees, are FDIC-insured in the United States. Your money is protected if the bank fails. Many fintech platforms lack equivalent protections.

Speed comparison tells the real story

Banks claim 1-5 business days. Often it’s 3-5. Fintech platforms promise same-day or next-day delivery. For urgent family situations, that matters.

But speed varies by destination country. Transfers to the Philippines historically move slower than transfers within Europe.

Security and regulatory status

Established banks face strict regulatory oversight. Every transfer is monitored. Fintech platforms vary dramatically:

- Some hold licenses from financial regulators

- Others partner with licensed banks (delegating responsibility)

- A few operate with minimal regulatory oversight

Always verify the fintech company’s regulatory status before sending money. Check if they’re licensed by the SEC, state money transmitter agencies, or equivalent bodies.

What matters for Filipino expatriates

Your family needs reliable, affordable transfers. Banks are reliable but expensive. Fintech platforms are cheaper but require more research into their legitimacy.

The sweet spot: fintech platforms that partner with regulated banks, offer transparent fees, and have positive user reviews specifically for Philippines transfers.

Fintech adopters can save 3-5% annually compared to traditional banks—on $6,000 annual remittances, that’s $180-300 extra reaching your family.

Hidden risks to watch

Some fintech platforms struggle with Philippine banking requirements. They require different documentation. Others have frozen accounts during compliance reviews. Ask whether the platform regularly transfers to your specific bank.

Exchange rate timing matters too. Some fintech platforms lock rates immediately; others wait hours. During volatile currency periods, that difference is significant.

Pro tip Send a small test transfer ($50-100) to any new fintech platform before transferring larger amounts—this reveals any hidden fees, delays, or documentation issues without risking substantial funds.

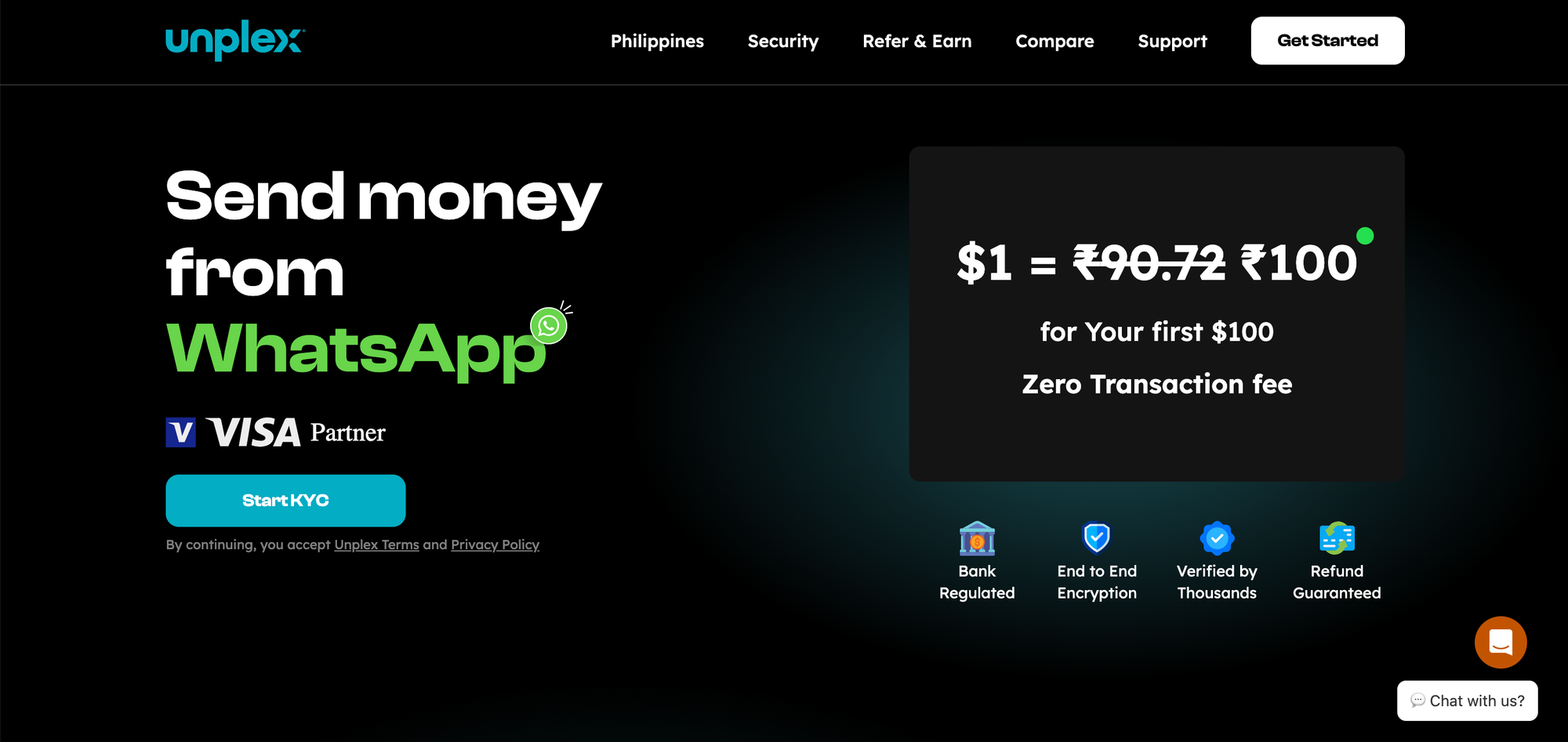

Save More on Your International Bank Transfers with Unplex

International money transfers to the Philippines can often feel complicated, costly, and slow. As the article explains, hidden fees, multiple intermediary banks, and unclear exchange rates all chip away at the amount your family actually receives. If you have experienced frustration with OUR fee structures, slow SWIFT transfers, or confusing compliance demands, you are not alone. Every dollar lost means less support for your loved ones.

Unplex offers a solution that directly addresses these pain points by providing quick, secure, and fee-free transfers using simple WhatsApp messaging. Our platform operates fully within regulated frameworks and partners with licensed banks to ensure your money moves safely and transparently. With Unplex, you can avoid costly hidden fees, enjoy instant transfers, and easily complete KYC requirements without hassle. Start maximizing the value of your remittances today by choosing a smarter alternative that Filipino expatriates trust.

Discover how easy and cost-effective sending money can be at Unplex. Explore our seamless setup and instant transfer benefits now by visiting https://unplex.money and experience the future of cross-border payments designed just for you.

Frequently Asked Questions

What factors affect the cost of international bank transfers?

The cost of international bank transfers is influenced by various factors, including the type of fee structure used (OUR, BEN, SHA), intermediary bank fees, and the exchange rate markup applied by the sending bank.

How do hidden fees impact the amount my family receives from a transfer?

Hidden fees can significantly reduce the amount your family receives. For example, a $500 transfer may only result in $480 received after all fees and markups are applied, leading to substantial annual losses without your knowledge.

Why do international transfers take longer when sending to certain locations?

International transfers take longer due to the routing process, which may involve multiple intermediary banks. Each transfer’s pathway varies significantly based on the destination and infrastructure in use, affecting speed.

What should I do to ensure my transfer is secure and compliant with regulations?

To ensure your transfer is secure, verify recipient details directly with your family before sending money. Additionally, be prepared to provide identification and purpose of funds to your bank to comply with KYC regulations.